003 / Flagship

Bank Advisor. Market intelligence at prompt speed.

Built on Saptiva Studio. The first market-intelligence copilot that runs inside the bank's own perimeter — where the private data already is. Public sector data. Regulatory context. The bank's own portfolio. Three sources. One prompt.

The product · bankadvisor.saptiva.com

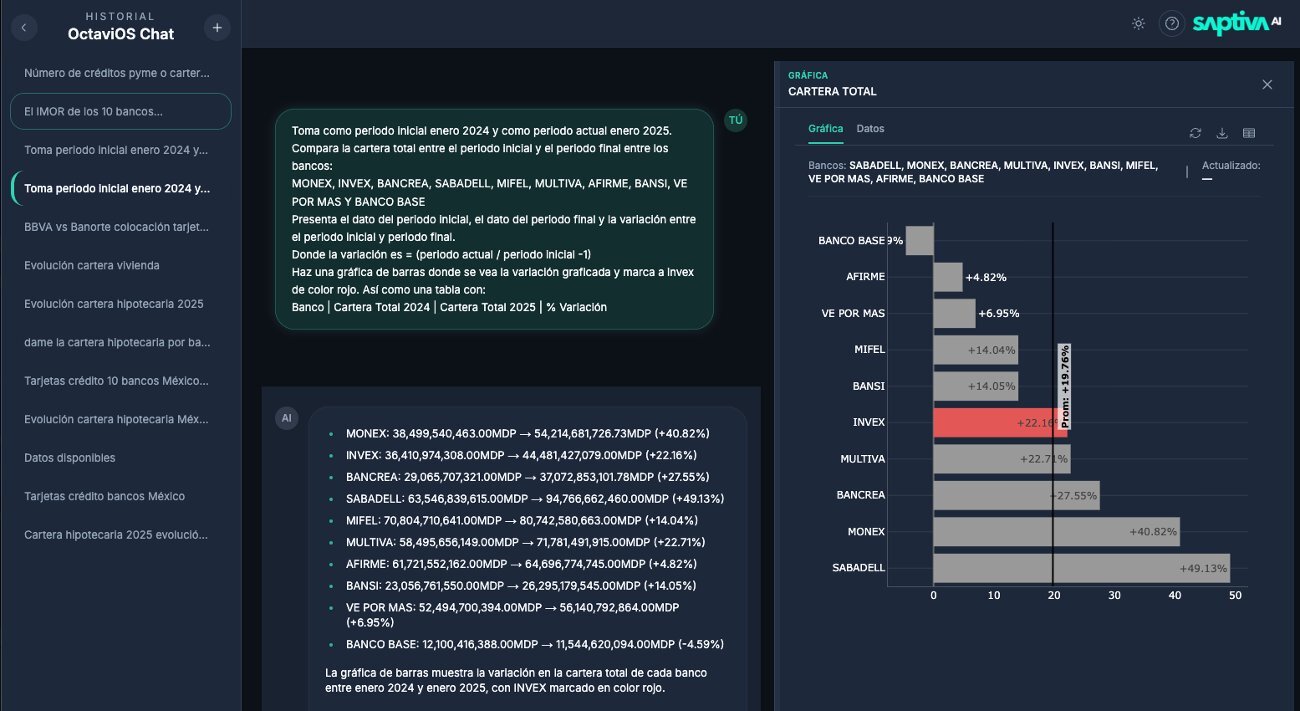

One prompt. Ten banks. Twelve months of market shift. The leadership asked for a cartera-total comparison across ten institutions, 2024 vs 2025 variation. The chart renders on the right. No analyst queue. No ticket. No week of waiting.

3–8Weeks of lag

Between the question the CEO asks and the market report that lands: up to eight weeks. By then the market moved. The analyst spent 70% of that time cleaning, joining, formatting. The data becomes context — never advantage.

Three sources · One context layer

01 / PUBLIC

The sector, ingested.

CNBV. Banxico. ABM. Credit bureaus. Portfolios, delinquency, rates, placement, deposits. The full public financial corpus — ingested, normalized, queryable.

02 / REGTECH

Bajaware makes it legible.

Regulatory taxonomy. Normative mapping. Live financial semantics. The context layer built by the RegTech that already serves the market — so the public data answers the questions a banker actually asks.

03 / PRIVATE

Your data never leaves.

Portfolio. Clients. Placement. Risk. Consulted in-place, with zero exfiltration. The model goes to the data, not the reverse. The bank's perimeter holds.

What the leadership asks — and gets answered, live.

Benchmarking

"Compare my credit-card portfolio against BBVA and Banorte. Last twelve months."

Sector evolution

"Mortgage portfolio evolution, 2025 vs 2024, by bank."

Risk & collection

"IMOR of the ten largest banks in the system. Flag deterioration."